The last couple of weeks have been fairly wild in insurtech and intermediated insurance.

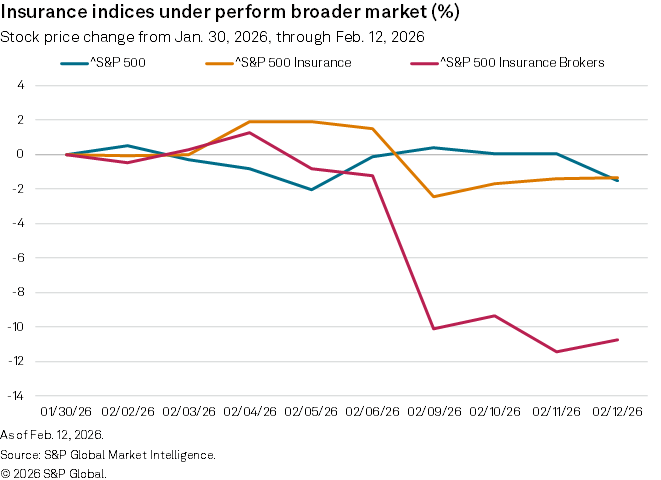

Two insurance apps went live inside ChatGPT, and caused global industry stocks to get whacked. I’m talking the S&P 500 Insurance Index down nearly 4% in a day, with big brokers like Willis Towers Watson off 12%, Gallagher around 10%, and Aon around 9%.

All because of one Spanish headquartered digital insurer and one US marketplace shipping V1 apps into an AI app store.

On the surface, this sounds ridiculous. But when you zoom out, I think it's actually the clearest signal we’ve had so far. Public markets now believe AI can sit between the customer and the traditional distribution stack. NOTE: There has been a bit of damage control since on the Insurify side.

This is not a micro change like we have seen in the past with distribution. It represents a step change (at least from a shareholder and the public market perspective)

DEEP DIVE: Here’s what actually happened (minus the hype)

A Spanish digital insurer, Tuio, got its home insurance app approved in the ChatGPT store.

That means any potential policyholder can now describe their home in normal language within ChatGPT, get a few clarifying questions, and then see a real quote - all without touching a portal or comparison site. Buying the policy is expected to follow (and OpenAI, Gemini, and the like have been introducing checkout and payment rails over the past few months).

Almost at the same time, Insurify launched what it calls the first insurance comparison app in the ChatGPT directory. It lets you research and compare car insurance options directly inside ChatGPT — personalised estimates, carrier reviews, likely pricing - all without jumping out to a website.

)

If you’ve worked in insurance for a while, none of this is alien. It’s quoting. It’s marketplace logic. It’s just happening in a different place.

Sound cool - but the part that seems bonkers is that brokers and intermediaries around the world had one of their worst trading days in years, as investors suddenly repriced the risk that AI could disintermediate parts of their model.

That’s the part that got me to the bigger realization. Not the “AI finally arrived” era - we’ve all been talking about this for years - but because of how fast (and brutal) the reaction was immediately after the announcement.

“We’ve had comparison sites for years. This is just Compare the Market inside ChatGPT. Calm down.”

Yeah and nah.

Yeah, marketplaces like Compare the Market have been steering personal lines for ages. They changed how motor and home get bought.

But what Tuio, Insurify (and the next wave) are doing is the agentic version of that model. That’s different in three important ways:

Old way: You go to a website, suffer through 40 fields, pray you don’t fat-finger something, then maybe get a list of quotes.

New way: You talk like a normal human - I've been preaching this north star to anyone I don't totally bore for a while.

“I’ve got a 2018 Corolla, do about 12,000 ks a year, one speeding ticket two years ago. Just moved houses. What do I actually need?”

The agent breaks that down, fills in the blanks, and comes back with structured data the rating engines can understand.

Potentially, the friction falls off a cliff. This applies to retail and business lines.

Old marketplace/comparison world:

Agentic world: the AI can

Previously, the transactional door to insurance was:

Now the front door is going to be the Agentic agent du jour (ChatGPT, Claude, Gemini, etc)

)

That matters because people don’t have to think “I’m going to go buy insurance” anymore. They can just say, “Hey, can you sort my car/home/business insurance?” from inside whatever the thing they are already using. And if that thing has a built-in agent or connection to a Broker Agent that knows how to shop the market.......it will, at scale

But I don't think this is the biggest part I want to highlight. These apps are V1s. It's the most primitive this tech will ever be, and it’s already good enough to move billions in market cap.

We're just scratching the surface. Two very specific flows went live:

That’s it. Personal lines, simple-ish risks, narrow journeys.

And that was enough to trigger the worst one-day fall in the S&P 500 Insurance Index since October, and double-digit hits for some of the biggest brokers on the planet.

Now imagine:

So what now? This is the point where I personally stop geeking out at this and start thinking about the back end.

Because all of these new front-end engagement points are only as good as the back ends they talk to and write to. If an AI agent tomorrow turned up at your virtual doorstep with a perfectly good risk and said:

“Quote this. Now bind it. And by the way, I’ll be back at renewal with three other options.”

…what happens inside your stack?

Can you:

For a lot of insurers, MGAs and brokers, the honest answer today is “no” or “only with a heroic amount of manual patching and jazz hand double entry.” That’s the bit that keeps niggling at me. The risk isn’t just “AI will disintermediate us”. The nearer-term risk is:

I’m not writing this from some smug “we’ve solved it” perspective. Coming back from a week hanging out with brokers, agencies, insurtechs, customers, and industry people, it's clear that InsuredHQ is not exempt from some serious sleeve rolling.

We’re well on the way - but we’ve got plenty more to do and plenty more we want to offer. The bar just went up, and it went up quickly this month.

If you’re a carrier, MGA, or broker, here’s a question I’d start with:

If an AI marketplace tried to send you business tomorrow (clean data, good risk, no bad claim history) - could you:

...and do it in real time without breaking your processes or losing the plot in your core systems?

If the answer is “no” or “only if someone manually keys it into three different places,” then maybe this is your wake-up call?

The front-end experience moved. Public markets noticed. And what shipped last week was only the tiniest taste of what agentic distribution will look like.

The job now is getting your stack – and your team – ready for that reality, not sitting on the sidelines hoping this all blows over.

-2.png?width=1200&length=1200&name=Untitled%20design%20(1)-2.png)

No Comments Yet

Let us know what you think